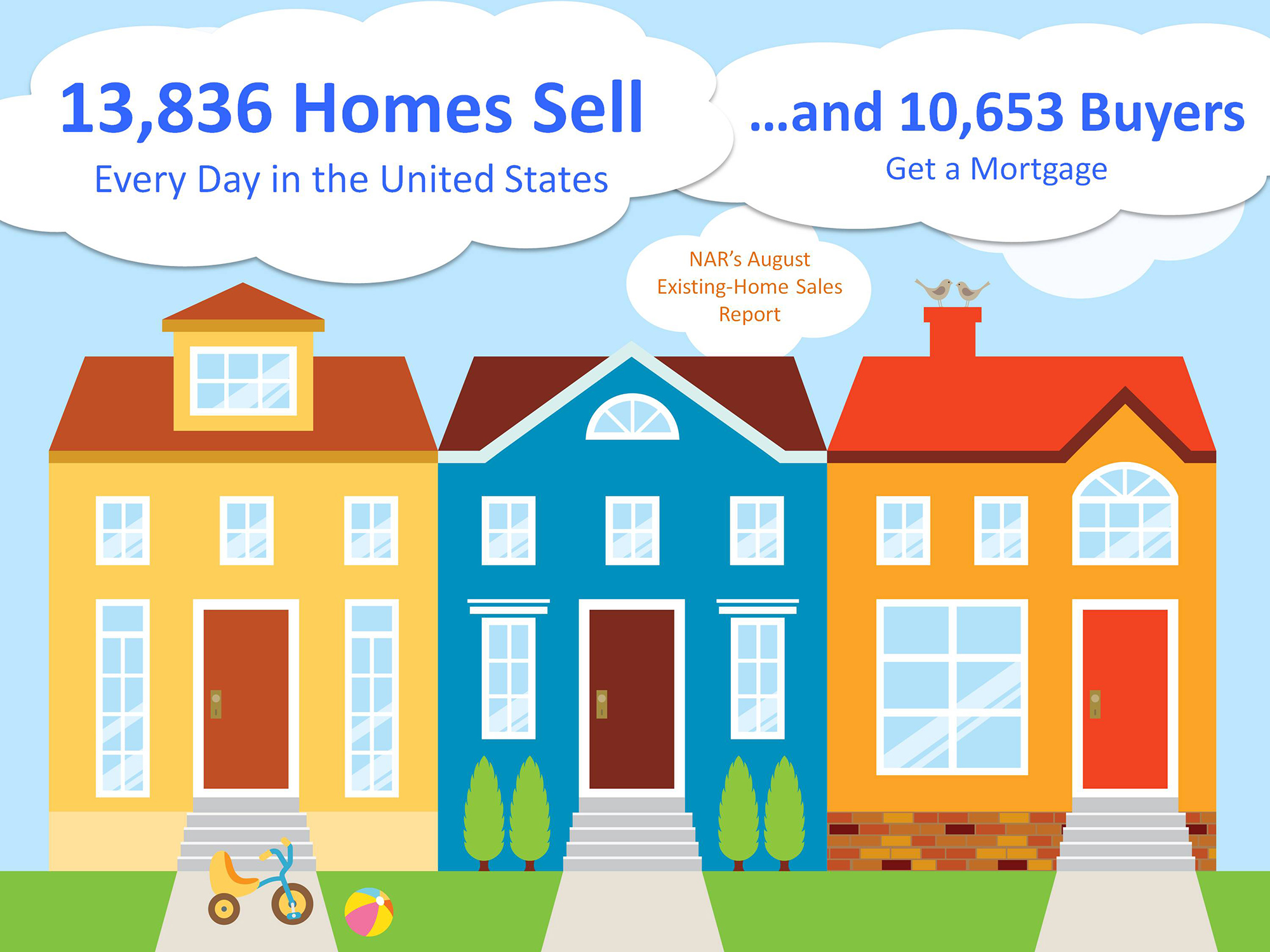

Most homeowners believe that the winter is not a good time to sell. This belief is based on the fact that historically the number of buyers decreases in the winter and then increases dramatically during the spring buying market. Though this is still true, there is an interesting pattern developing over the last few months.

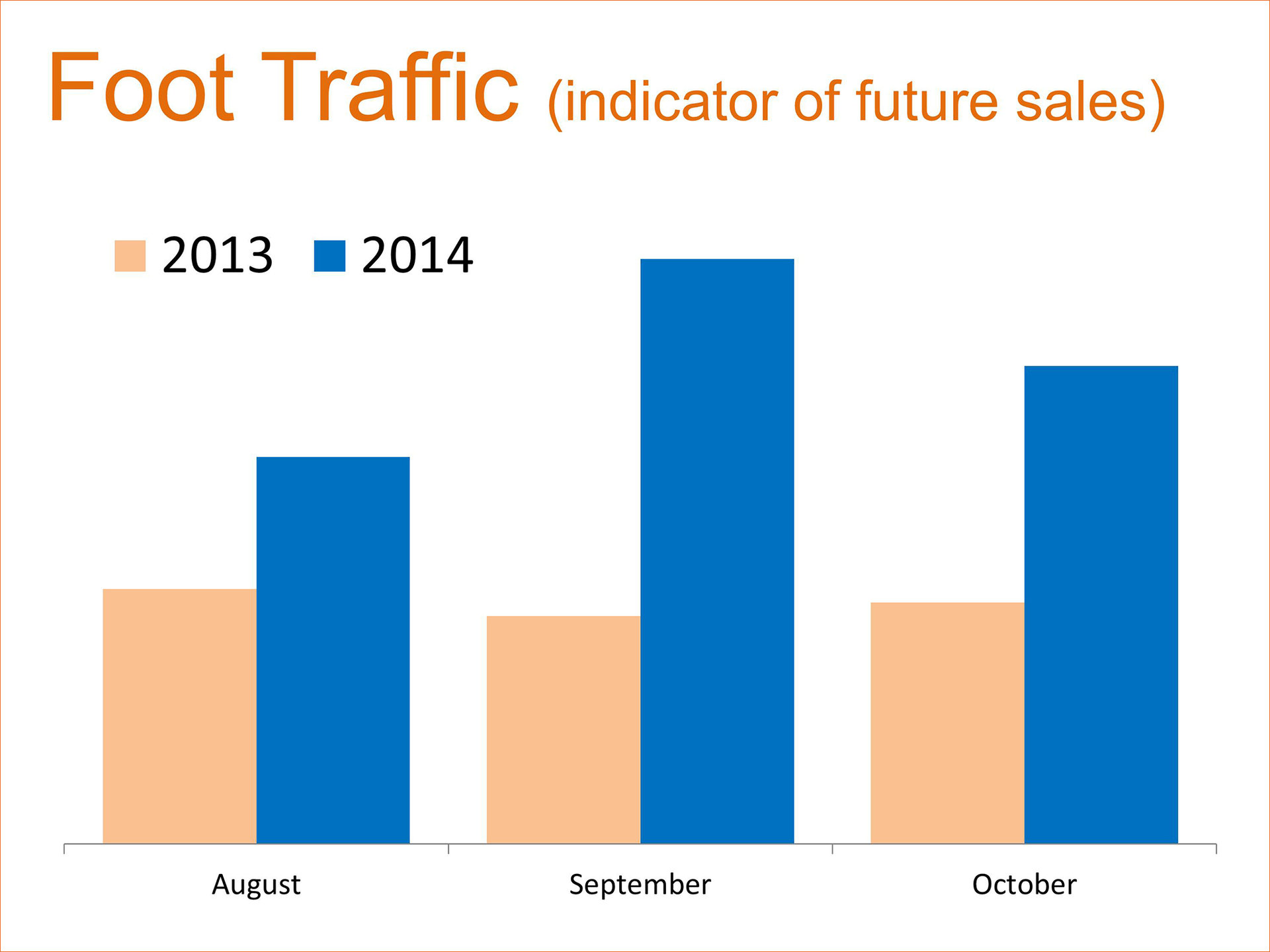

The number of prospective purchasers actively looking at a home (foot traffic) has remained strong going into the fall. As a matter of fact, the foot traffic far exceeds the numbers reported for the same months last year (see chart):

Most homeowners believe that the winter is not a good time to sell. This belief is based on the fact that historically the number of buyers decreases in the winter and then increases dramatically during the spring buying market. Though this is still true, there is an interesting pattern developing over the last few months.

The number of prospective purchasers actively looking at a home (foot traffic) has remained strong going into the fall. As a matter of fact, the foot traffic far exceeds the numbers reported for the same months last year (see chart):

Proof that NOW is a Good Time to Sell

Most homeowners believe that the winter is not a good time to sell. This belief is based on the fact that historically the number of buyers decreases in the winter and then increases dramatically during the spring buying market. Though this is st...

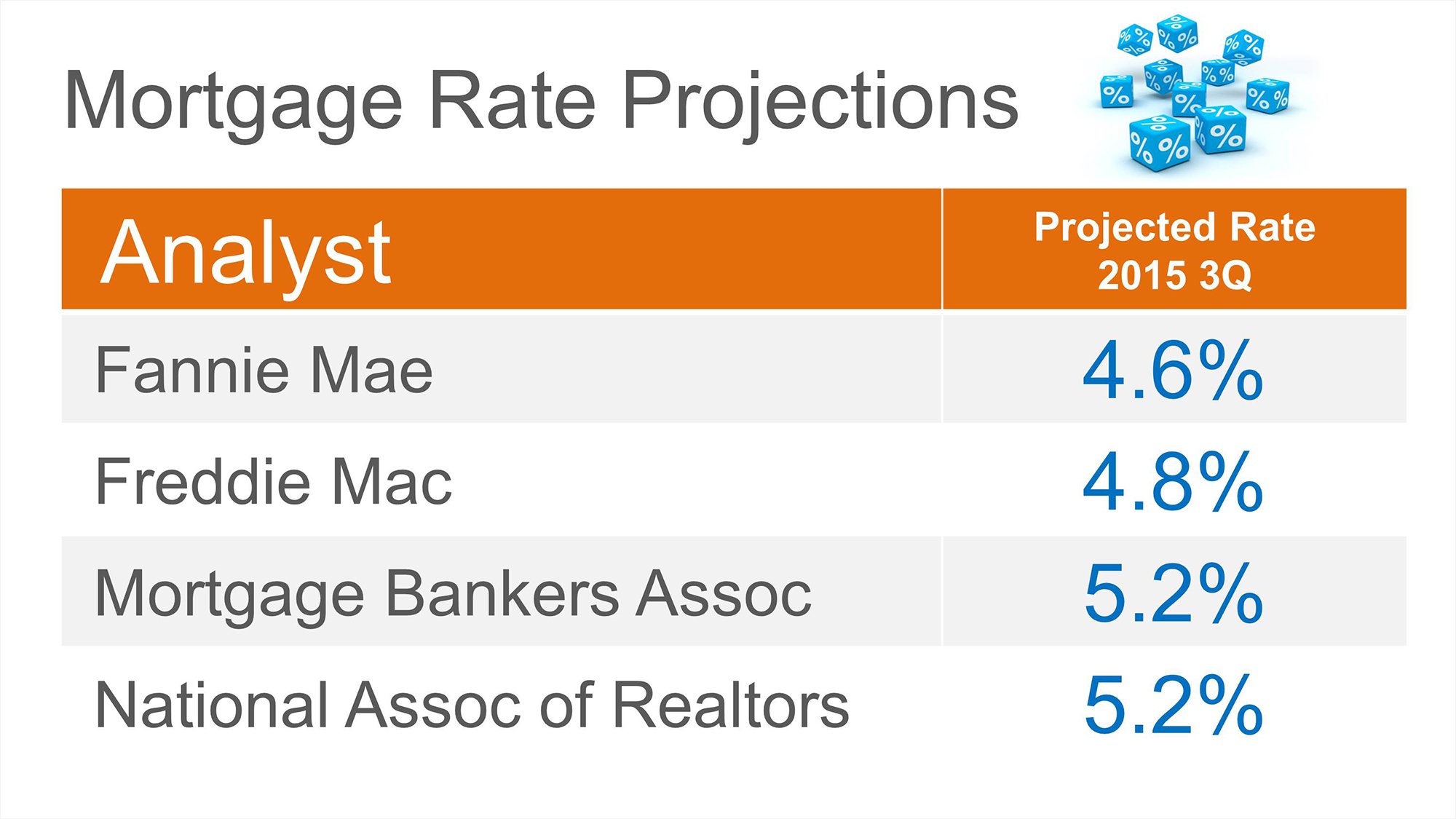

Today, many real estate conversations center on housing prices and where they may be headed. That is why we like the Home Price Expectation Survey.

Every quarter, Pulsenomics surveys a nationwide panel of over one hundred economists, real estate experts and investment & market strategists about where prices are headed over the next five years. They then average the projections of all 100+ experts into a single number.

Today, many real estate conversations center on housing prices and where they may be headed. That is why we like the Home Price Expectation Survey.

Every quarter, Pulsenomics surveys a nationwide panel of over one hundred economists, real estate experts and investment & market strategists about where prices are headed over the next five years. They then average the projections of all 100+ experts into a single number.

Today, many real estate conversations center on housing prices and where they may be headed. That is why we like the Home Price Expectation Survey.

Every quarter, Pulsenomics surveys a nationwide panel of over one hundred economists, real estate experts and investment & market strategists about where prices are headed over the next five years. They then average the projections of all 100+ experts into a single number.

Today, many real estate conversations center on housing prices and where they may be headed. That is why we like the Home Price Expectation Survey.

Every quarter, Pulsenomics surveys a nationwide panel of over one hundred economists, real estate experts and investment & market strategists about where prices are headed over the next five years. They then average the projections of all 100+ experts into a single number.

Eric Belsky is Managing Director of the Joint Center of Housing Studies at Harvard University. He also currently serves on the editorial board of the Journal of Housing Research and Housing Policy Debate. Last year, he released a paper on homeownership -

Eric Belsky is Managing Director of the Joint Center of Housing Studies at Harvard University. He also currently serves on the editorial board of the Journal of Housing Research and Housing Policy Debate. Last year, he released a paper on homeownership -  Eric Belsky is Managing Director of the Joint Center of Housing Studies at Harvard University. He also currently serves on the editorial board of the Journal of Housing Research and Housing Policy Debate. Last year, he released a paper on homeownership -

Eric Belsky is Managing Director of the Joint Center of Housing Studies at Harvard University. He also currently serves on the editorial board of the Journal of Housing Research and Housing Policy Debate. Last year, he released a paper on homeownership -  After it was announced that Fannie Mae and Freddie Mac would again make available mortgage loans requiring as little as a

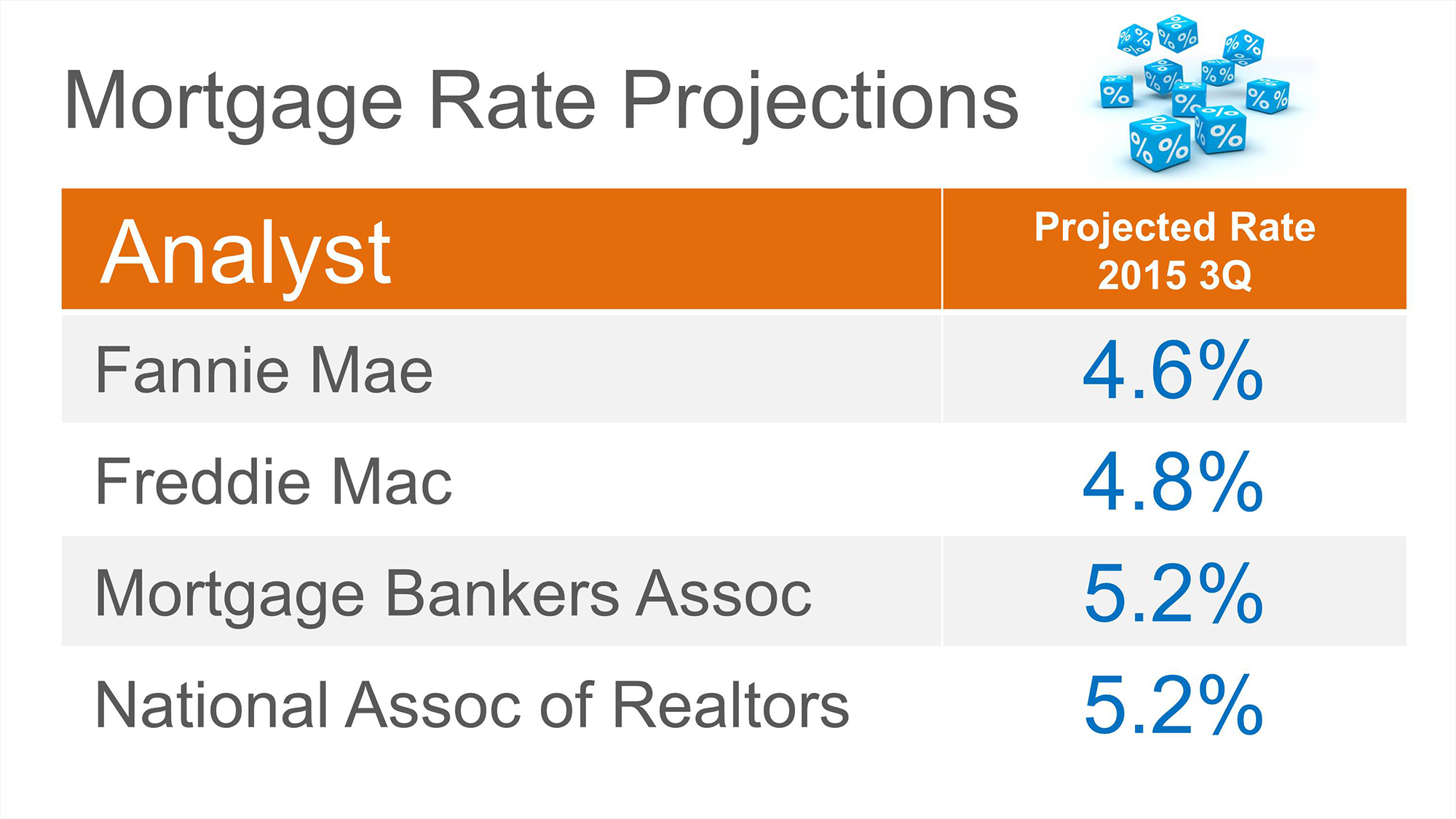

After it was announced that Fannie Mae and Freddie Mac would again make available mortgage loans requiring as little as a

A

A  Some homeowners may consider trying to sell their home on without the assistance of a real estate professional, known in the industry as a For Sale by Owner (FSBO). We think there are several reasons this might not be a good idea for the vast majority of sellers.

Some homeowners may consider trying to sell their home on without the assistance of a real estate professional, known in the industry as a For Sale by Owner (FSBO). We think there are several reasons this might not be a good idea for the vast majority of sellers.

There are some homeowners that have been waiting for months to get a price they hoped for when they originally listed their house for sale. The only thing they might want to consider is... If it hasn't sold yet this fall, maybe it's not priced properly.

There are some homeowners that have been waiting for months to get a price they hoped for when they originally listed their house for sale. The only thing they might want to consider is... If it hasn't sold yet this fall, maybe it's not priced properly.

There are some homeowners that have been waiting for months to get a price they hoped for when they originally listed their house for sale. The only thing they might want to consider is... If it hasn't sold yet this fall, maybe it's not priced properly.

There are some homeowners that have been waiting for months to get a price they hoped for when they originally listed their house for sale. The only thing they might want to consider is... If it hasn't sold yet this fall, maybe it's not priced properly.

If you are thinking about purchasing a home right now, you are surely getting a lot of advice. Though your friends and family have your best interests at heart, they may not be fully aware of your needs and what is currently happening in real estate. Let’s look at whether or not now is actually a good time for you to buy a home.

There are three questions you should ask before purchasing in today’s market:

If you are thinking about purchasing a home right now, you are surely getting a lot of advice. Though your friends and family have your best interests at heart, they may not be fully aware of your needs and what is currently happening in real estate. Let’s look at whether or not now is actually a good time for you to buy a home.

There are three questions you should ask before purchasing in today’s market:

Billionaire money manager John Paulson was

Billionaire money manager John Paulson was  Do you really need an agent to sell your house in today’s market? Here’s what Fannie Mae suggests to sellers on the

Do you really need an agent to sell your house in today’s market? Here’s what Fannie Mae suggests to sellers on the  In real estate there is a difference between COST and PRICE. As a seller, you will be most concerned about ‘short term price’ – where home values are headed over the next six months. As either a first time or repeat buyer, you must not be concerned about price but instead about the ‘long term cost’ of the home.

In real estate there is a difference between COST and PRICE. As a seller, you will be most concerned about ‘short term price’ – where home values are headed over the next six months. As either a first time or repeat buyer, you must not be concerned about price but instead about the ‘long term cost’ of the home.

Two recently released reports indicate that both young adults (Millennials) and teenagers (Generation Z) still see homeownership as an important piece of their future success.

A report by The Demand Institute,

Two recently released reports indicate that both young adults (Millennials) and teenagers (Generation Z) still see homeownership as an important piece of their future success.

A report by The Demand Institute,

In a recent survey,

In a recent survey,  With interest rates still in the

With interest rates still in the

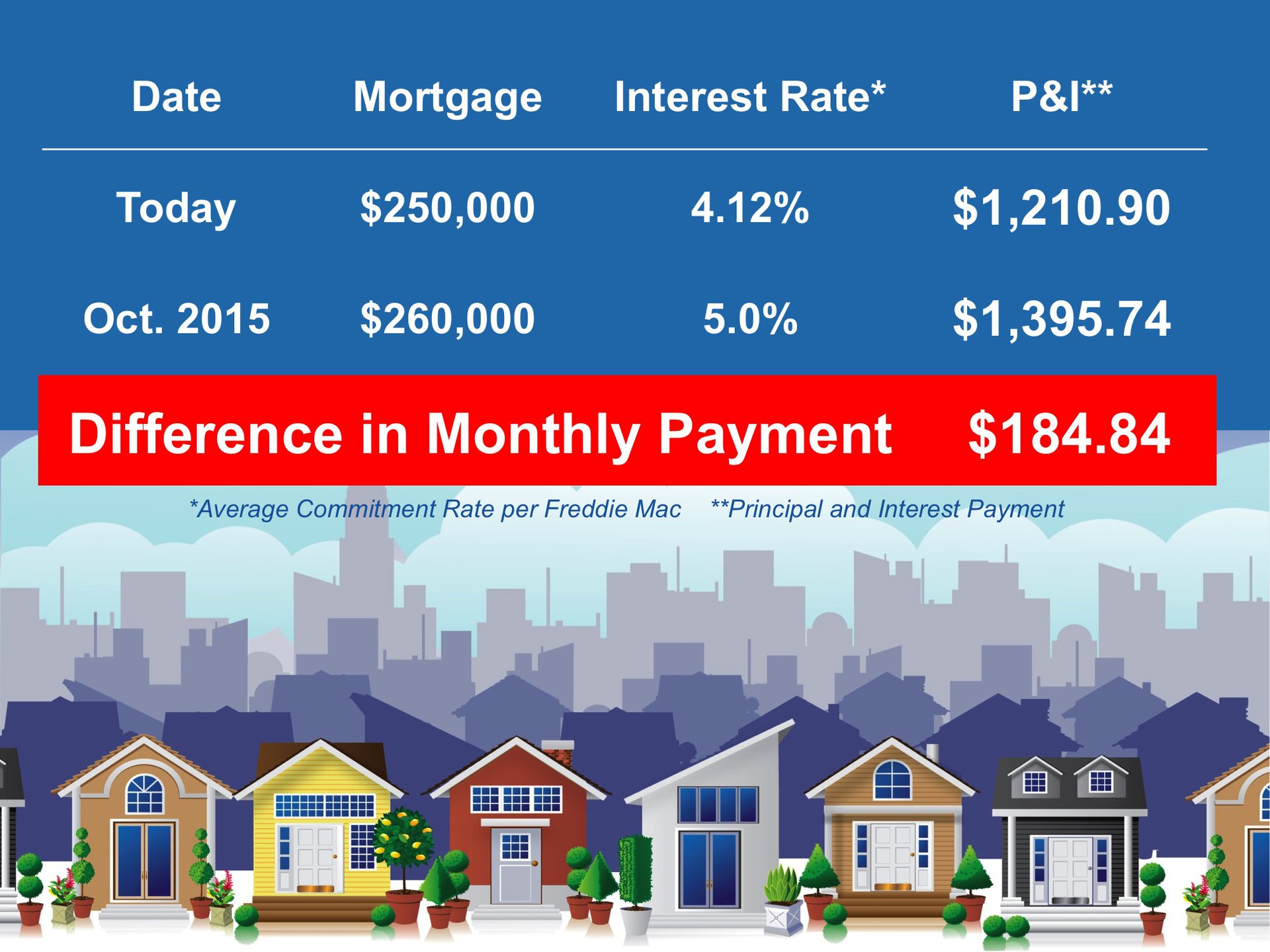

We are often asked why there is so much paperwork mandated by the bank for a mortgage loan application when buying a home today. It seems that the bank needs to know everything about us and requires three separate sources to validate each and every entry on the application form. Many buyers are being told by friends and family that the process was a hundred times easier when they bought their home ten to twenty years ago.

There are two very good reasons that the loan process is much more onerous on today’s buyer than perhaps any time in history.

We are often asked why there is so much paperwork mandated by the bank for a mortgage loan application when buying a home today. It seems that the bank needs to know everything about us and requires three separate sources to validate each and every entry on the application form. Many buyers are being told by friends and family that the process was a hundred times easier when they bought their home ten to twenty years ago.

There are two very good reasons that the loan process is much more onerous on today’s buyer than perhaps any time in history.

[assets] => Array

(

)

[can_share] => no

[categories] => Array

(

[0] => stdClass Object

(

[category_type] => standard

[children] =>

[created_at] => 2019-06-03T18:18:43Z

[id] => 1

[name] => Uncategorized

[parent] =>

[parent_id] =>

[published_at] => 2019-06-03T18:18:43Z

[slug] => uncategorized

[status] => public

[translations] => stdClass Object

(

[es] => stdClass Object

(

[name] => No clasificado

)

)

[updated_at] => 2019-06-03T18:18:43Z

)

)

[content_type] => blog

[contents] =>

[assets] => Array

(

)

[can_share] => no

[categories] => Array

(

[0] => stdClass Object

(

[category_type] => standard

[children] =>

[created_at] => 2019-06-03T18:18:43Z

[id] => 1

[name] => Uncategorized

[parent] =>

[parent_id] =>

[published_at] => 2019-06-03T18:18:43Z

[slug] => uncategorized

[status] => public

[translations] => stdClass Object

(

[es] => stdClass Object

(

[name] => No clasificado

)

)

[updated_at] => 2019-06-03T18:18:43Z

)

)

[content_type] => blog

[contents] =>