- The Home Price Expectation Survey says that prices will appreciate by 5.8% this year.

- The Freddie Mac Outlook Report is looking for home prices to appreciate by around 7% in 2018.

- The CoreLogic HPI Forecast indicates that home prices will increase by 5.2% on a year-over-year basis.

Bottom Line

As Freddie Mac reported earlier this year in their Insights Report, “Nowhere to go but up? How increasing mortgage rates could affect housing,”“As mortgage rates increase, the demand for home purchases will likely remain strong relative to the constrained supply and continue to put upward pressure on home prices.”[created_at] => 2018-05-31T06:00:00Z [description] => Mortgage interest rates have increased by more than half of a point since the beginning of the year. They are projected to increase by an additional half of a point by year’s end. Because of this increase in rates, some are guessing that home prices will depreciate. [expired_at] => [featured_image] => https://files.simplifyingthemarket.com/wp-content/uploads/2018/05/30104847/20180531-Share-STM.jpg [id] => 1097 [published_at] => 2018-05-31T10:00:00Z [related] => Array ( ) [slug] => will-home-prices-fall-as-mortgage-rates-rise [status] => published [tags] => Array ( ) [title] => Will Home Prices Fall as Mortgage Rates Rise? [updated_at] => 2018-05-30T12:44:34Z [url] => /2018/05/31/will-home-prices-fall-as-mortgage-rates-rise/ )

Will Home Prices Fall as Mortgage Rates Rise?

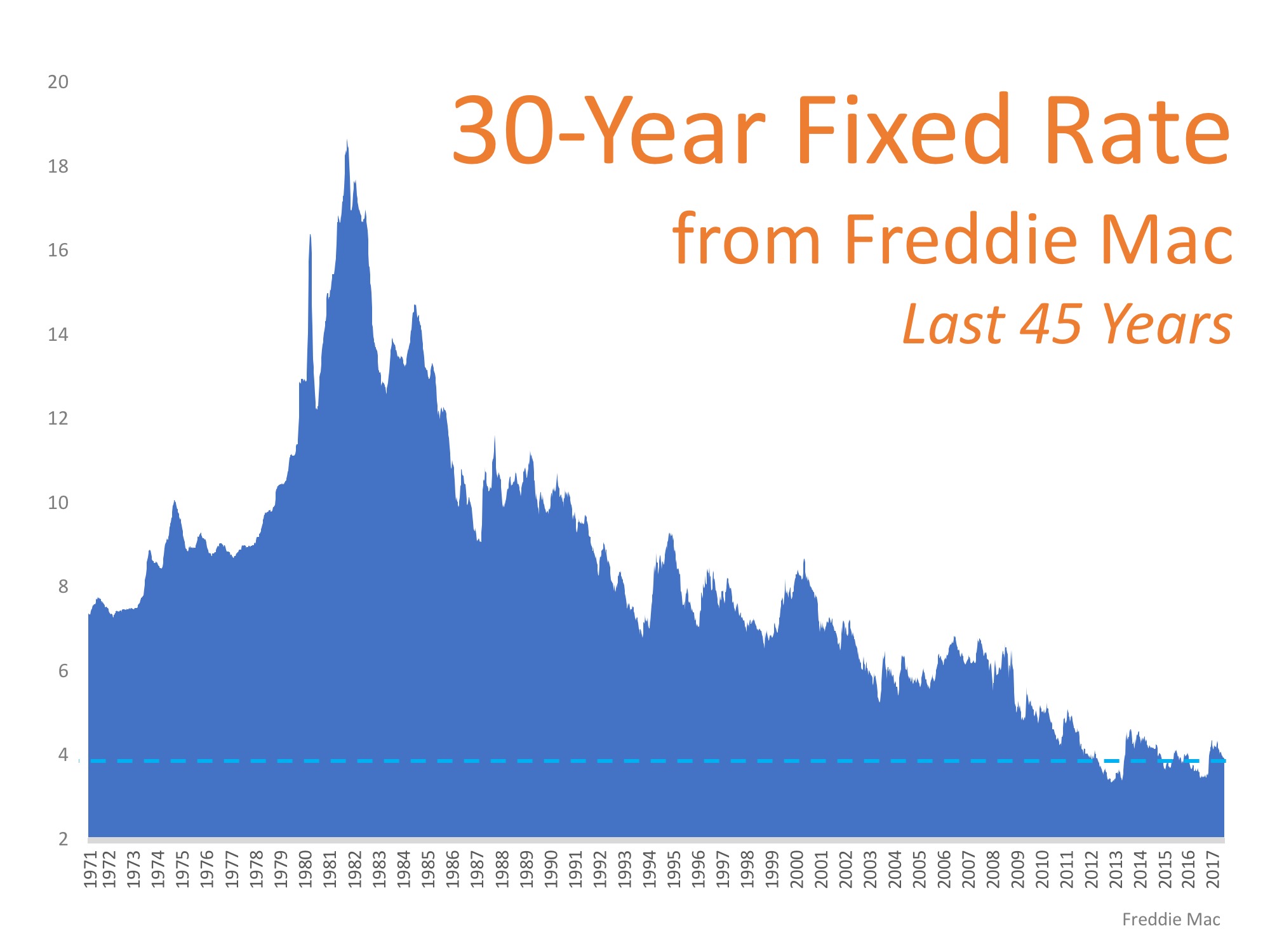

Mortgage interest rates have increased by more than half of a point since the beginning of the year. They are projected to increase by an additional half of a point by year’s end. Because of this increase in rates, some are guessing that home prices will depreciate.

![Home Buying Myths Slayed [INFOGRAPHIC] | Simplifying the Market](https://files.keepingcurrentmatters.com/wp-content/uploads/2018/04/20180420-STM-ENG.jpg)

![Buying a Home Can Be Scary... Unless You Know the Facts [INFOGRAPHIC] | Simplifying The Market](https://files.keepingcurrentmatters.com/wp-content/uploads/2017/10/Mythbusters-STM.jpg)

![Home Buying Myths Slayed [INFOGRAPHIC] | Simplifying the Market](https://files.keepingcurrentmatters.com/wp-content/uploads/2017/07/Slaying-Myths-STM.jpg)

![Slaying Home Buying Myths [INFOGRAPHIC] | Simplifying the Market](https://files.keepingcurrentmatters.com/wp-content/uploads/2017/04/Slaying-Myths-STM-2.jpg)