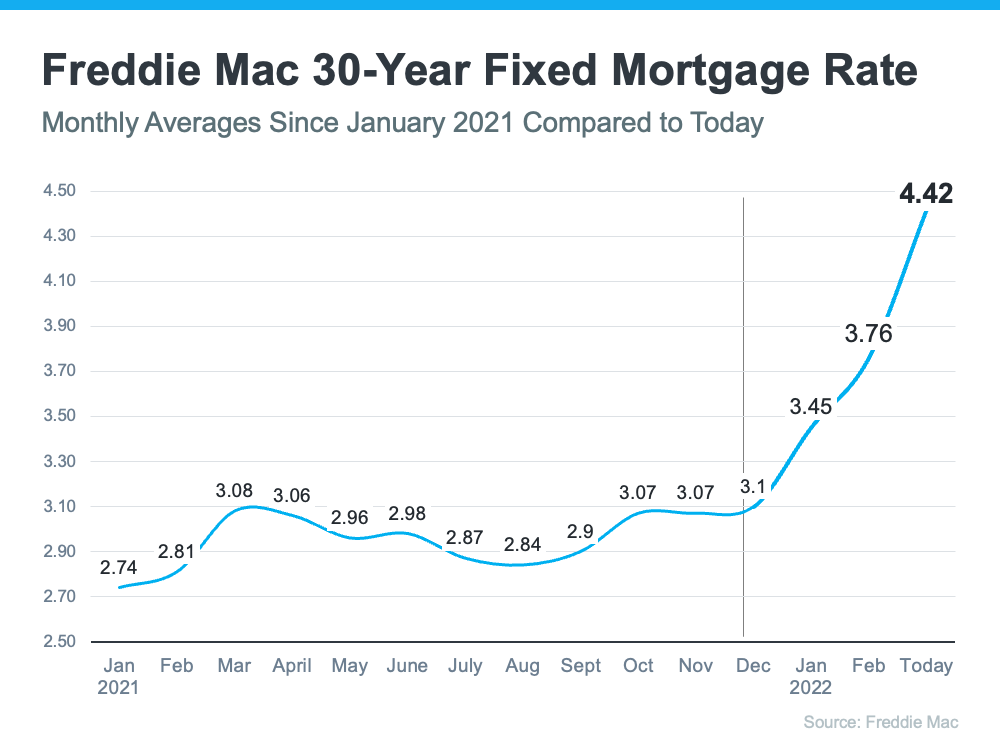

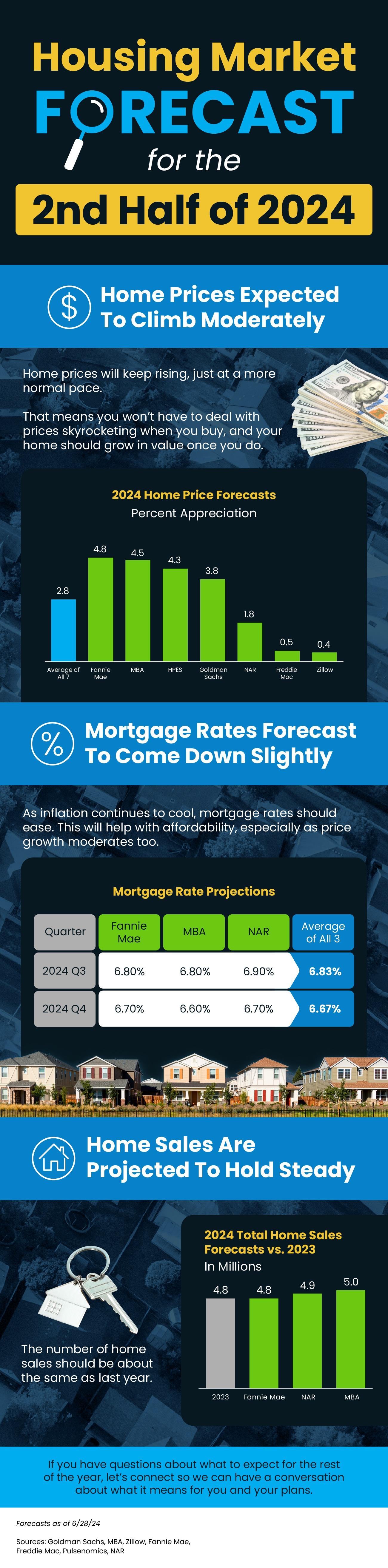

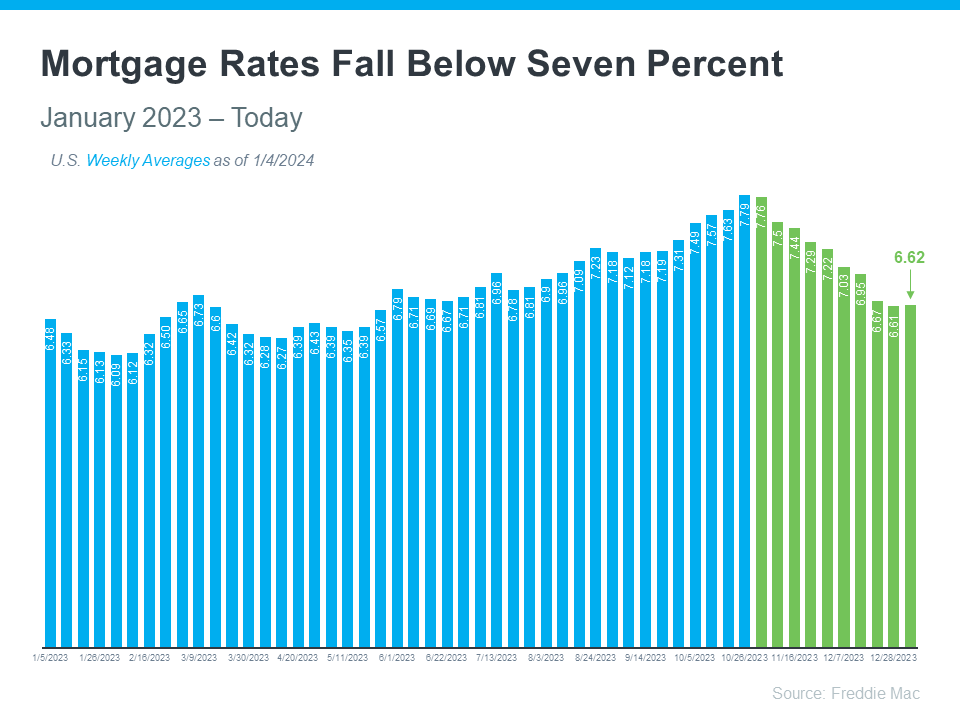

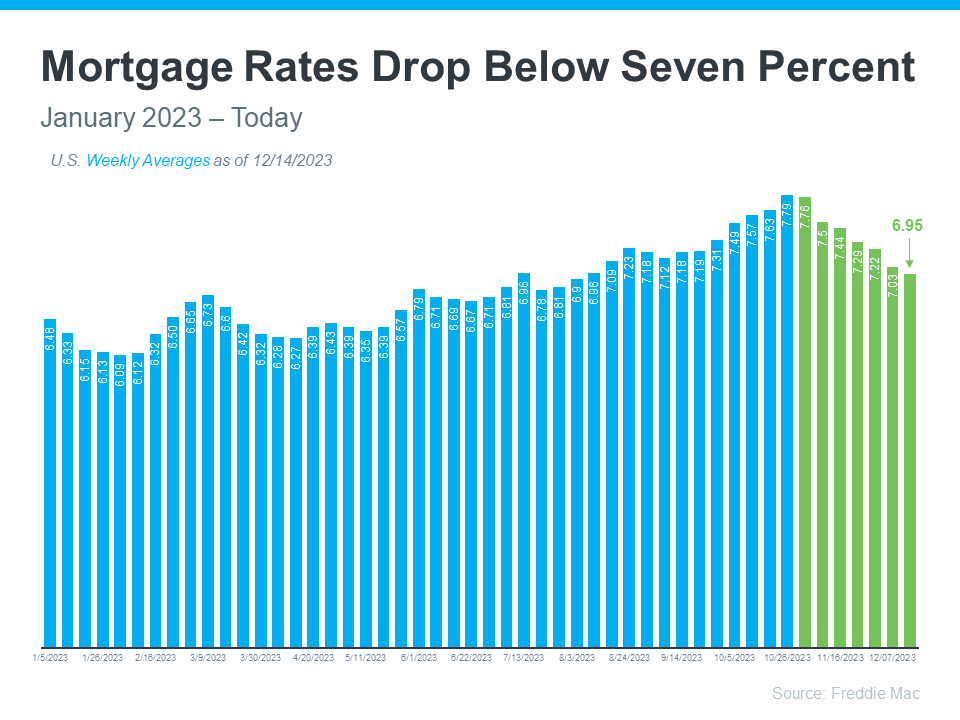

- Wondering what the second half of the year holds for the housing market? Here’s what expert forecasts say.

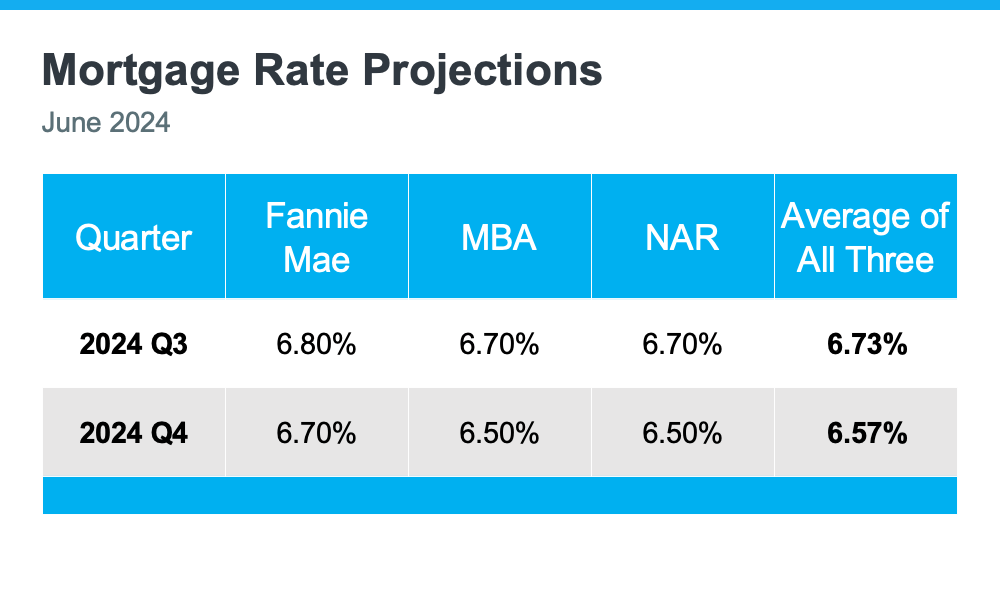

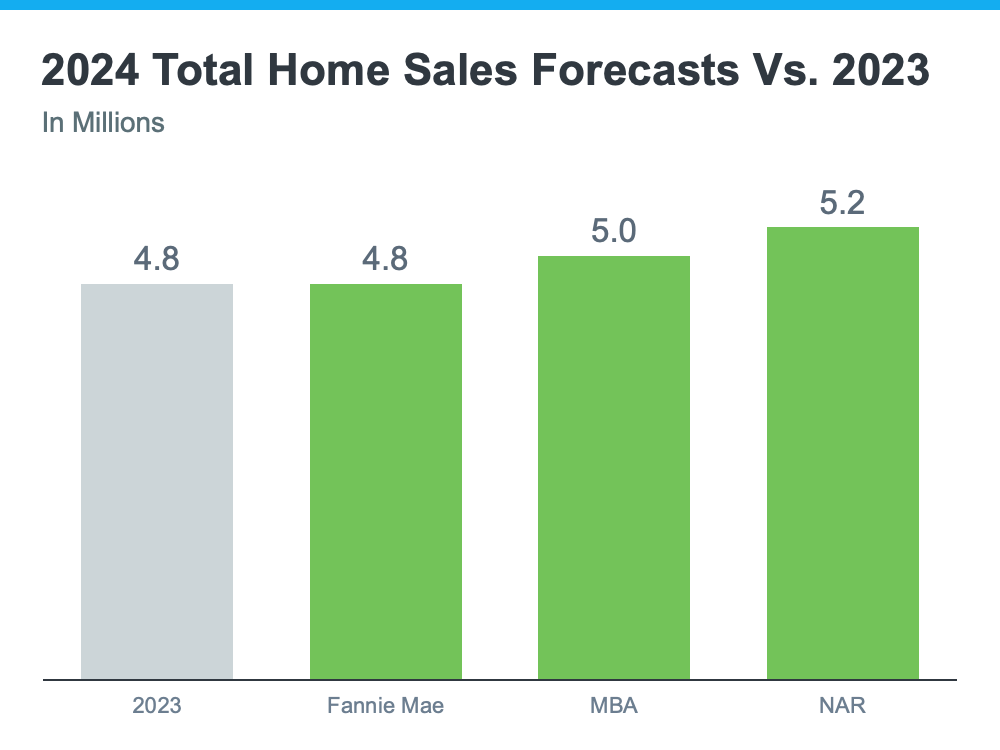

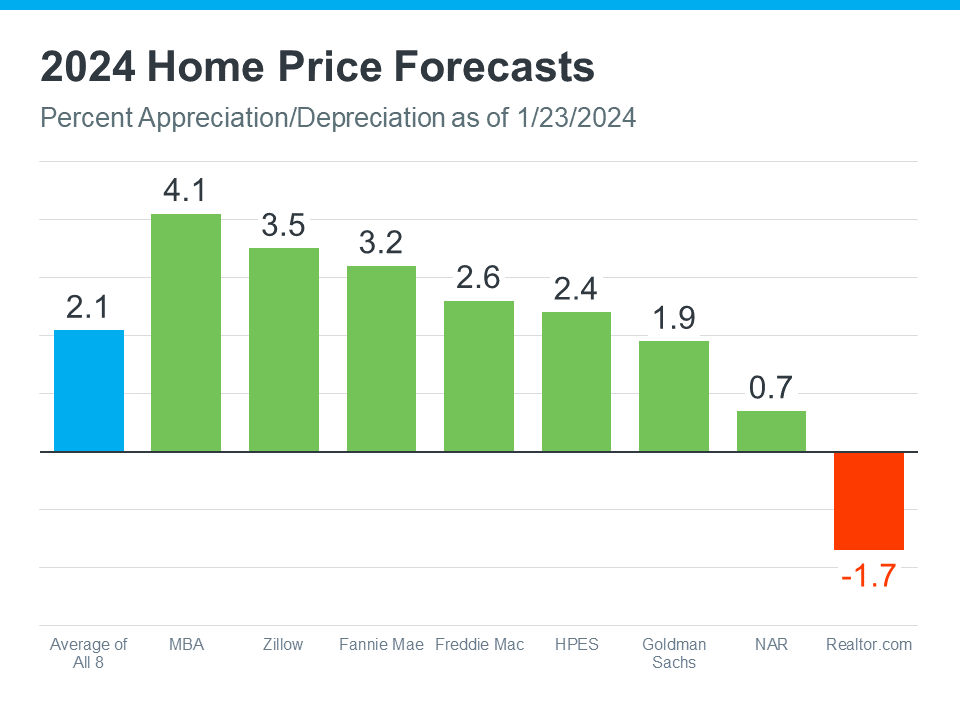

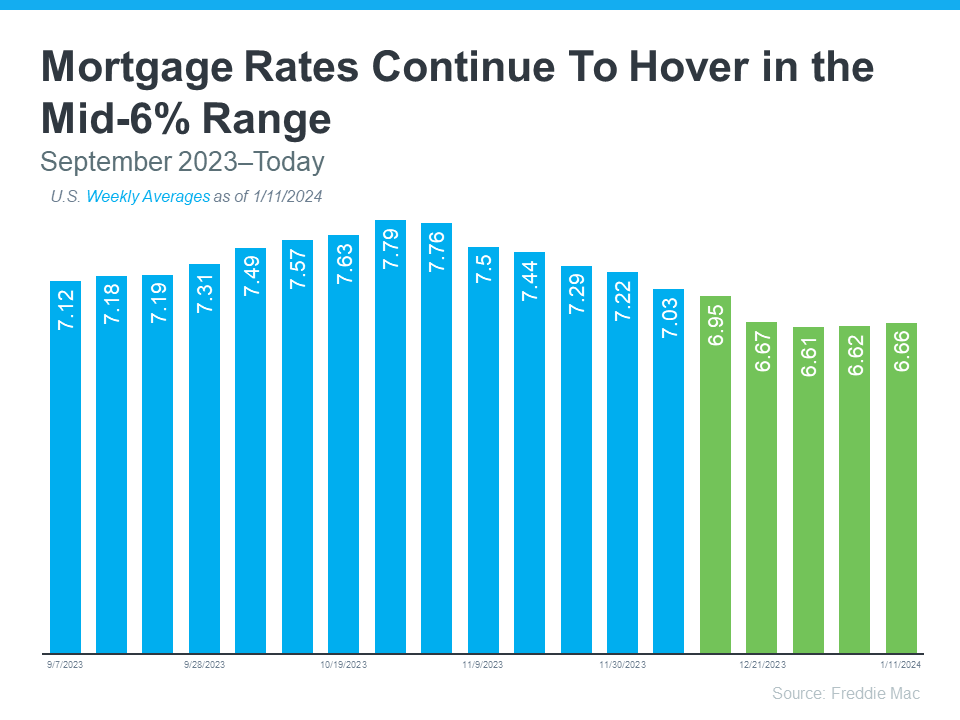

- Home prices are expected to climb moderately. Mortgage rates are forecast to come down slightly. And, home sales are projected to hold steady.

- If you have questions about what to expect for the rest of the year, let’s connect so we can have a conversation about what it means for you and your plans.

Wondering what the second half of the year holds for the housing market? Here’s what expert forecasts say.

[exclusive_id] => [expired_at] => [featured_image] => https://files.keepingcurrentmatters.com/KeepingCurrentMatters/content/images/20240627/Housing-Market-Forecast-for-the-2nd-Half-of-2024-KCM-Share-original.png [id] => 55688 [kcm_ig_caption] => Wondering what the second half of the year holds for the housing market? Here’s what expert forecasts say. Home prices are expected to climb moderately. Mortgage rates are forecast to come down slightly. And, home sales are projected to hold steady. If you have questions about what to expect for the rest of the year, DM me so we can have a conversation about what it means for you and your plans. [kcm_ig_hashtags] => stayinformed,staycurrent,keepingcurrentmatters [kcm_ig_quote] => Housing market forecast for the 2nd half of 2024. [public_bottom_line] =>- Wondering what the second half of the year holds for the housing market? Here’s what expert forecasts say.

- Home prices are expected to climb moderately. Mortgage rates are forecast to come down slightly. And, home sales are projected to hold steady.

- If you have questions about what to expect for the rest of the year, connect with a local agent to have a conversation about what it means for you and your plans.

Housing Market Forecast for the 2nd Half of 2024 [INFOGRAPHIC]

Wondering what the second half of the year holds for the housing market? Here’s what expert forecasts say.

![What Is Multigenerational Housing? [INFOGRAPHIC] | Simplifying The Market](https://files.keepingcurrentmatters.com/wp-content/uploads/2022/04/20220415-MEM.png)