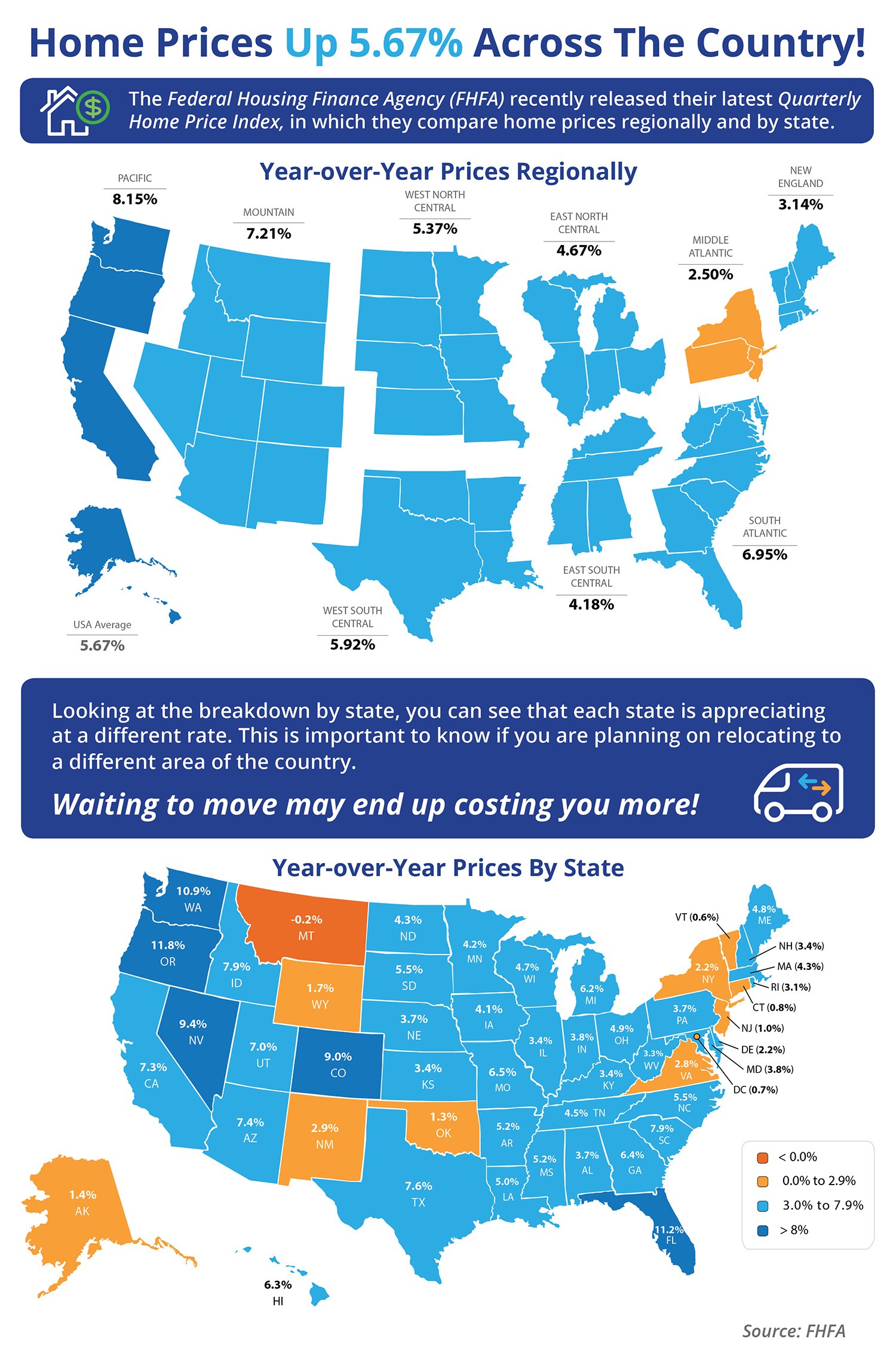

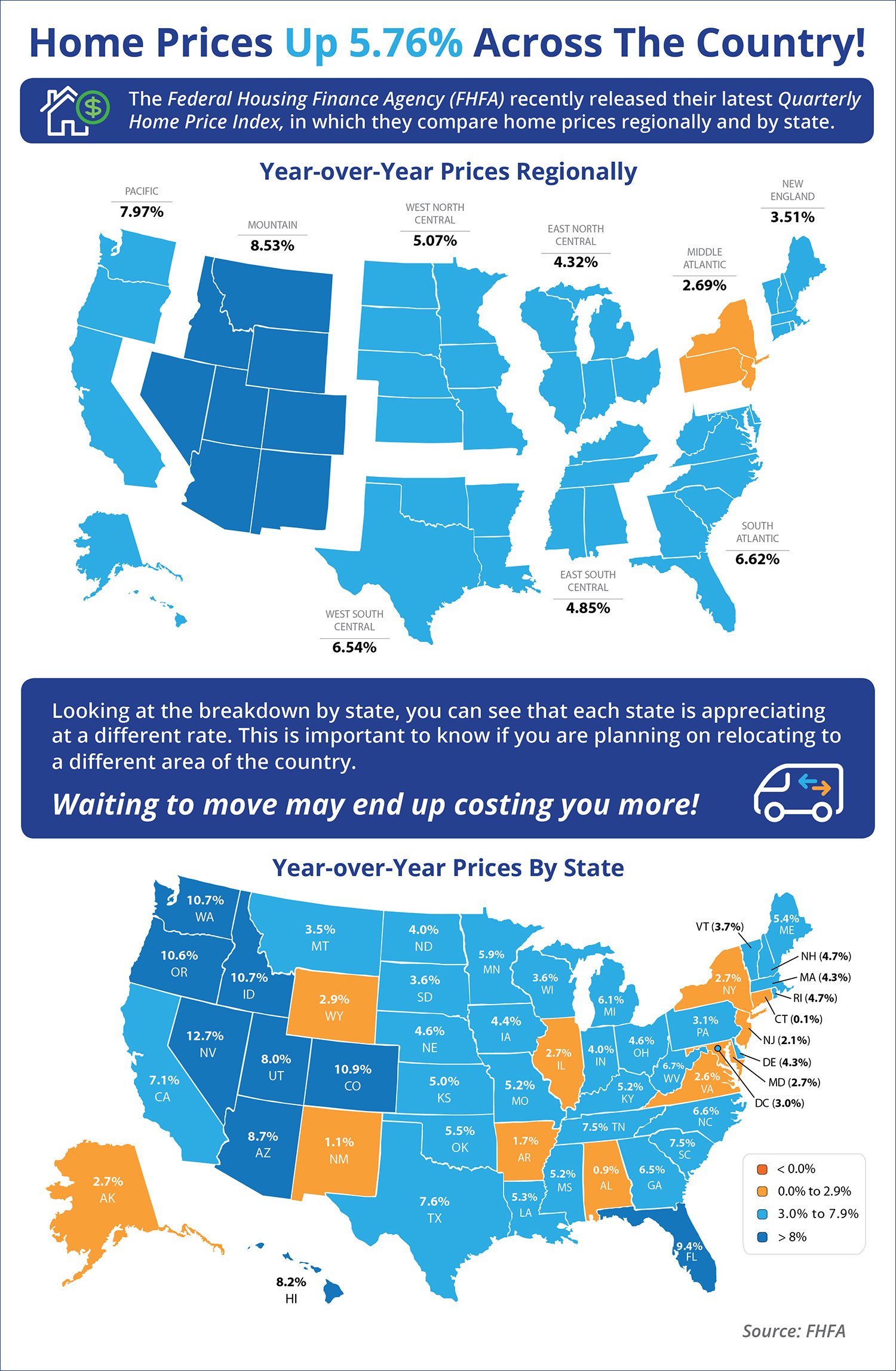

Home Prices Up 5.67% Across The Country! [INFOGRAPHIC]

Some Highlights:

- Across the country, home prices are up by 5.67%.

- Each state is appreciating at a different rate, however, which is important to realize if you plan on relocating to a different state.

- Regionally, prices have appreciated year-over-year by as high as 8.15%.

![The Difference An Hour Makes This Spring [INFOGRAPHIC] | Simplifying The Market](https://files.keepingcurrentmatters.com/wp-content/uploads/2016/02/The-Difference-a-Hour-Makes-STM.jpg)

![Existing Home Sales Bounce Back [INFOGRAPHIC] | Simplifying The Market](https://files.keepingcurrentmatters.com/wp-content/uploads/2016/01/EHS-JAN-STM.jpg)

![Should I Buy Now Or Wait Until Next Year? [INFOGRAPHIC] | Simplifying The Market](https://files.keepingcurrentmatters.com/wp-content/uploads/2016/01/Cost-of-Waiting-STM.jpg)