The National Association of Realtors just released their

The National Association of Realtors just released their - Vacation-home sales catapulted to an estimated 1.13 million last year

- This was the highest amount since NAR began the survey in 2003

- Vacation sales were up 57.4% from 717,000 in 2013

- Vacation-home sales accounted for 21 percent of all transactions in 2014, their highest market share since the survey was first conducted

Bottom Line

If you have been considering a waterfront condo at the beach, that ranch in the foothills or that special getaway you someday will retire to, maybe now is the time to act. Prices are good and mortgage rates are at historic lows. Contact a local real estate professional to help you put your dreams to a plan. [created_at] => 2015-04-14T06:00:50Z [description] => The National Association of Realtors just released their 2015 Investment and Vacation Home Buyers Survey which revealed that vacation home sales boomed in 2014 to above their most recent peak level in 2006. NAR Chief Economist Lawrence Yun sai... [expired_at] => [featured_image] => https:/// [id] => 277 [published_at] => 2015-04-14T10:00:50Z [related] => Array ( ) [slug] => desire-to-own-a-vacation-home-growing [status] => published [tags] => Array ( ) [title] => Desire to Own a Vacation Home Growing [updated_at] => 2015-04-15T11:42:21Z [url] => /2015/04/14/desire-to-own-a-vacation-home-growing/ )Desire to Own a Vacation Home Growing

The National Association of Realtors just released their 2015 Investment and Vacation Home Buyers Survey which revealed that vacation home sales boomed in 2014 to above their most recent peak level in 2006.

NAR Chief Economist Lawrence Yun sai...

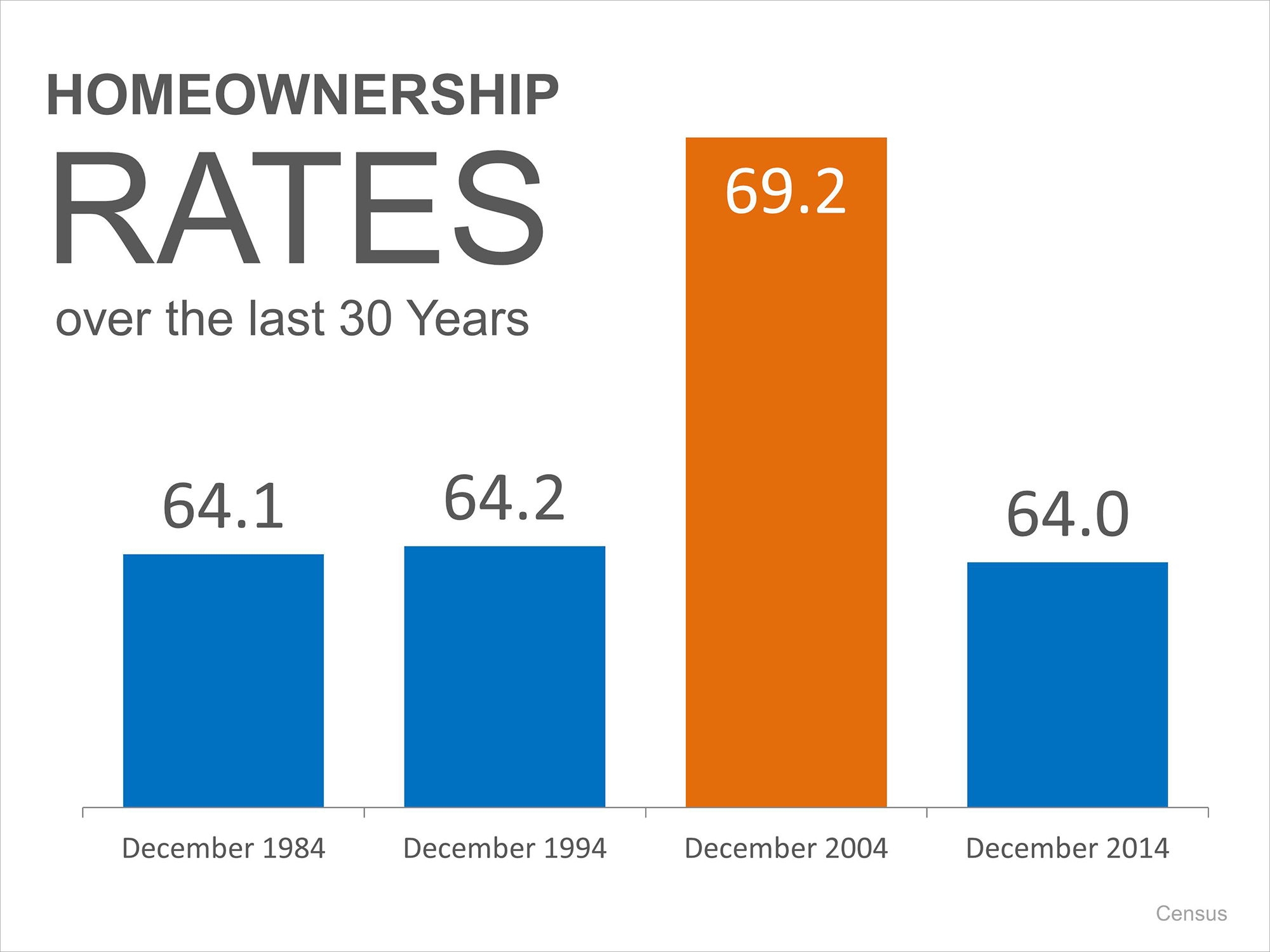

The Census recently released their 2014 Homeownership Statistics, and many began to worry that Americans have taken a step back from the notion of homeownership.

The Census recently released their 2014 Homeownership Statistics, and many began to worry that Americans have taken a step back from the notion of homeownership.

The headlines agree mortgage interest rates have dropped substantially below initial projections. Many who are considering purchasing a home, or moving up to their dream home, might think that they should wait to buy, because rates may continue to fall.

A recent

The headlines agree mortgage interest rates have dropped substantially below initial projections. Many who are considering purchasing a home, or moving up to their dream home, might think that they should wait to buy, because rates may continue to fall.

A recent  A

A

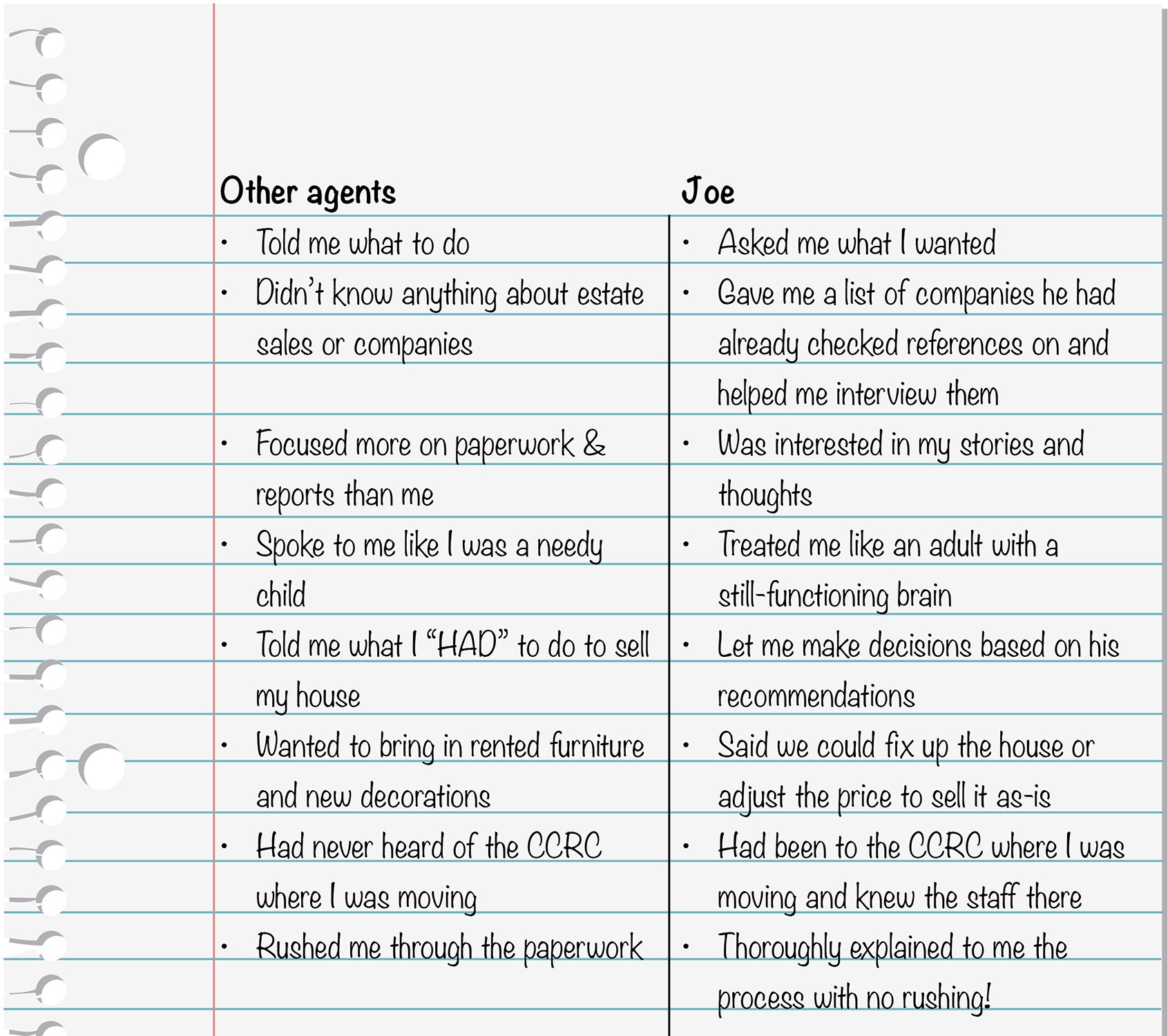

Whether you are buying or selling a home, the process can be challenging. That is why you should take on the services of a real estate professional when embarking on a potential home move. However, not all real estate agents are the same. A family must make sure they hire someone who truly understands the current housing market and, not only that, knows how to connect the dots to explain how market conditions may impact your decision.

How can you make sure you have an agent who meets these requirements?

Here are just a few questions every real estate professional should be able to answer for their clients and customers:

Whether you are buying or selling a home, the process can be challenging. That is why you should take on the services of a real estate professional when embarking on a potential home move. However, not all real estate agents are the same. A family must make sure they hire someone who truly understands the current housing market and, not only that, knows how to connect the dots to explain how market conditions may impact your decision.

How can you make sure you have an agent who meets these requirements?

Here are just a few questions every real estate professional should be able to answer for their clients and customers:

There are some pundits lamenting the softness of the 2014 housing market. We can’t understand why. Though it is true that the early part of the year disappointed because of a myriad of reasons (ex. weather, lack of inventory, less distressed sales), the recent housing news is extremely encouraging. Let’s give some examples:

There are some pundits lamenting the softness of the 2014 housing market. We can’t understand why. Though it is true that the early part of the year disappointed because of a myriad of reasons (ex. weather, lack of inventory, less distressed sales), the recent housing news is extremely encouraging. Let’s give some examples:

Every day we are pleasantly surprised with the research coming forward regarding the Millennial generation. Whether it was

Every day we are pleasantly surprised with the research coming forward regarding the Millennial generation. Whether it was

For almost a year now, we have been trying to debunk the myth that student debt is keeping the vast majority of Millennials from purchasing a home.

We explained that Millennials have purchased more homes over a recent twelve month period than any other generation as was

For almost a year now, we have been trying to debunk the myth that student debt is keeping the vast majority of Millennials from purchasing a home.

We explained that Millennials have purchased more homes over a recent twelve month period than any other generation as was  Many sellers are still hesitant about putting their house up for sale. Where are prices headed? Where are interest rates headed? Can buyers qualify for a mortgage? These are all valid questions. However, there are several reasons to sell your home sooner rather than later. Here are five of those reasons.

Many sellers are still hesitant about putting their house up for sale. Where are prices headed? Where are interest rates headed? Can buyers qualify for a mortgage? These are all valid questions. However, there are several reasons to sell your home sooner rather than later. Here are five of those reasons.

Do as I Say… not as I Do

Do as I Say… not as I Do Growing up it seemed ‘white lies’ were okay while lying was a sin. As children, we sometimes had difficulty understanding where the line was. As we matured, we realized there most definitely was a difference.

Growing up it seemed ‘white lies’ were okay while lying was a sin. As children, we sometimes had difficulty understanding where the line was. As we matured, we realized there most definitely was a difference. Someone said to me recently, “Sixty-five is the new forty-five.” We chuckled, but the more I thought about it, the more I found myself in full agreement.

With more and more people working beyond traditional retirement age and the advances in modern medicine, the lines between middle and late adulthood are becoming a bit blurred.

Someone said to me recently, “Sixty-five is the new forty-five.” We chuckled, but the more I thought about it, the more I found myself in full agreement.

With more and more people working beyond traditional retirement age and the advances in modern medicine, the lines between middle and late adulthood are becoming a bit blurred.

Millennials have become an important topic of discussion for media outlets and blogs throughout the Country. While some argue that my generation is blossoming later than our predecessors, optimists such as myself believe that with our rebounding economy will help Millennials finally arrive in the economic arena that allows them the growth potential generations before us were afforded.

While I truly believe Millennials are positioned to become an important force in the new economy, the widening economic policy that minimizes retirement accounts and creates underemployment of Millennials threatens what is now America’s largest demographic.

Millennials have become an important topic of discussion for media outlets and blogs throughout the Country. While some argue that my generation is blossoming later than our predecessors, optimists such as myself believe that with our rebounding economy will help Millennials finally arrive in the economic arena that allows them the growth potential generations before us were afforded.

While I truly believe Millennials are positioned to become an important force in the new economy, the widening economic policy that minimizes retirement accounts and creates underemployment of Millennials threatens what is now America’s largest demographic.

Nielsen recently released their report “

Nielsen recently released their report “